Understanding the Benefits and Limitations of ACA Plans: A Comprehensive Guide

Brief insight

The Affordable Care Act (ACA), also known as Obamacare, created health insurance marketplaces where individuals and small businesses can shop for health insurance plans. ACA plans offer essential health benefits, such as preventive care and maternity care, and are required to cover pre-existing conditions. There are four levels of ACA plans based on the level of cost-sharing between the individual and the insurance company, with the most popular being silver plans. However, ACA plans can have limitations such as narrow provider networks and high out-of-pocket costs.

PHOTO: www.2020mom.org

ACA Plans: Access to Quality Healthcare

The Affordable Care Act (ACA), also known as Obamacare, was signed into law in 2010 with the aim of expanding access to quality healthcare for Americans. One of the key components of the ACA is the creation of health insurance marketplaces, where individuals and small businesses can shop for health insurance plans.

ACA plans are health insurance plans that are available through these marketplaces. They are designed to make healthcare more affordable and accessible for Americans who may not have employer-sponsored health insurance or who cannot afford to purchase health insurance on their own.

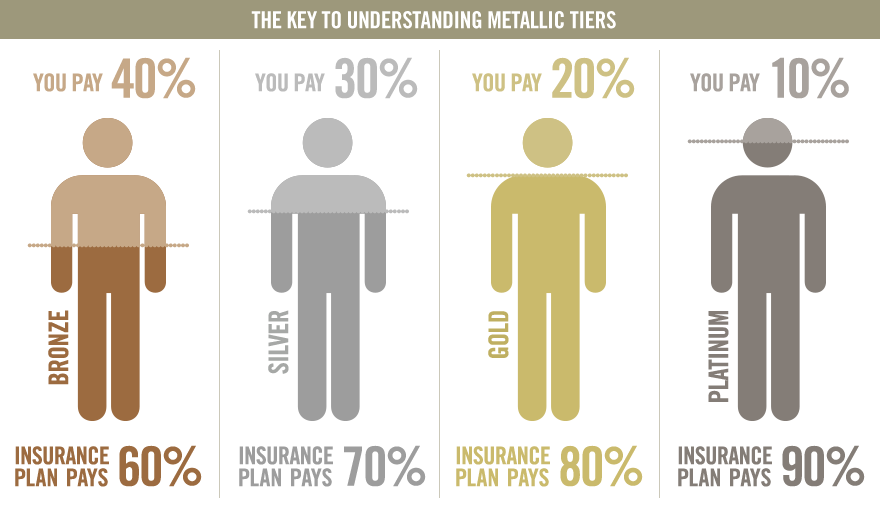

There are four levels of ACA plans: bronze, silver, gold, and platinum. The levels are based on the level of cost-sharing between the individual and the insurance company. Bronze plans have the lowest premiums but the highest out-of-pocket costs, while platinum plans have the highest premiums but the lowest out-of-pocket costs.

All ACA plans provide essential health benefits, such as preventive care, emergency services, hospitalization, prescription drug coverage, and mental health and substance abuse treatment. Insurance companies are also required to cover pre-existing conditions and cannot charge higher premiums based on an individual's health status.

One of the most popular types of ACA plans is the silver plan. Silver plans offer moderate premiums and cost-sharing and are eligible for cost-sharing reductions based on income. These subsidies can help reduce out-of-pocket costs such as deductibles, copays, and coinsurance.

However, ACA plans can have limitations such as narrow provider networks and high out-of-pocket costs. It is important for individuals to carefully review and compare their options when choosing an ACA plan to ensure they select a plan that meets their healthcare needs and budget.

Last Trends in ACA plans

The Biden-Harris Administration announces that more than 16.3 million people have enrolled in an Affordable Care Act (ACA) Marketplace health plan during the 2023 Marketplace Open Enrollment Period, which ran from November 1, 2022, to January 15, 2023, for most Marketplaces. This year, 22% of total enrollees were new to the Marketplaces, representing a 21% increase in new-to-Marketplace plan selections compared to last year. The article also highlights the unprecedented investment in the ACA by the Biden-Harris Administration, which has led to record-breaking enrollment numbers and an all-time low in the national uninsured rate. The highly competitive Marketplace, the availability of new standardized plan options, and the expanded financial assistance have contributed to increased enrollment.

Understanding ACA Plans: Coverage and Benefits

The Affordable Care Act (ACA) offers four types of health insurance plans - bronze, silver, gold, and platinum - that differ in terms of coverage and cost-sharing. Here's a detailed overview of each plan.

PHOTO: mnjinsurance.com

Bronze Plan

Bronze plans have the lowest monthly premiums but the highest out-of-pocket costs among the four ACA plan categories. They cover about 60% of healthcare expenses on average, leaving the other 40% to be paid out-of-pocket by the insured person.

Bronze plans typically have a higher deductible, which is the amount you have to pay for covered medical expenses before the insurance starts paying, compared to silver, gold, and platinum plans. The annual deductible for a bronze plan in 2021 is $6,000 for an individual and $12,000 for a family.

After meeting the deductible, the insurance company will pay for covered medical services, but the insured person will still have to pay a coinsurance or copayment for each service received. Coinsurance is a percentage of the cost of the service that the insured person must pay, while a copayment is a fixed amount.

While bronze plans have higher out-of-pocket costs, they still provide the essential health benefits required by the ACA, such as preventive care, prescription drugs, and emergency services. Additionally, people under the age of 30 and those who qualify for a hardship exemption can purchase a catastrophic health plan, which has even lower monthly premiums than a bronze plan but covers only essential health benefits and has a high deductible.

Bronze plans are best suited for individuals or families who are generally healthy and do not anticipate needing a lot of medical services throughout the year. However, if you have a chronic health condition or expect to need frequent medical care, a silver, gold, or platinum plan may provide better coverage and lower out-of-pocket costs.

Silver plan

The ACA silver plan is one of four metal-level plans available on the health insurance marketplace. It provides moderate coverage with affordable monthly premiums and out-of-pocket costs. The silver plan typically covers around 70% of a person's healthcare expenses, with the remaining 30% covered by the individual. The exact coverage and costs of a silver plan may vary depending on the state and insurance provider.

One of the key benefits of the silver plan is that it qualifies for cost-sharing reductions, which can lower the out-of-pocket costs for eligible individuals. These reductions are based on income and can lower the deductibles, copayments, and coinsurance for medical services.

The silver plan also covers essential health benefits, including preventive care, prescription drugs, and mental health services. Preventive care services are typically covered in full, meaning no out-of-pocket costs for the individual. However, prescription drug coverage may require a copayment or coinsurance.

The silver plan is a popular choice for individuals who want moderate coverage at an affordable cost. It may be a good option for those who qualify for cost-sharing reductions or who have a moderate amount of healthcare needs.

Last Trends in ACA plans

Mental health coverage: Many ACA plans have expanded coverage for mental health services, recognizing the growing need for these services during the pandemic. This includes coverage for therapy, counseling, and other mental health treatments.

Gold plan

The ACA Gold plan is a type of health insurance plan offered on the Health Insurance Marketplace that provides a high level of coverage for medical expenses. It is more expensive than the Bronze and Silver plans but offers lower out-of-pocket costs and higher coverage limits.

Under the ACA Gold plan, the insurance company pays for 80% of covered medical expenses, while the insured person is responsible for the remaining 20%. This means that the gold plan has a higher monthly premium compared to Bronze and Silver plans, but lower deductibles, copayments, and coinsurance.

The Gold plan is designed for individuals who anticipate using healthcare services frequently, such as those with chronic conditions or who require regular medical treatment. It covers essential health benefits, such as preventive care, prescription drugs, and mental health services, as required by the ACA.

In addition to the higher level of coverage, the Gold plan also offers the possibility of cost-sharing reductions for individuals with low to moderate incomes. These subsidies reduce out-of-pocket costs, such as deductibles and copayments, making healthcare more affordable for those who need it the most.

However, it is important to note that the ACA Gold plan may not be the best choice for everyone. It is typically more expensive than other plans, and individuals should carefully consider their healthcare needs and budget before selecting a plan. Additionally, the availability of Gold plans may vary by state and region, and not all insurers offer them.

Platinum

The ACA platinum plan is the highest level of coverage and provides the most comprehensive benefits, with the lowest out-of-pocket costs. Platinum plans have the highest monthly premiums of all the ACA plans, but they offer the most generous coverage for medical expenses.

Under the platinum plan, insurers are required to cover at least 90% of the cost of covered health services, with the policyholder responsible for the remaining 10%. This means that for every $100 in covered medical expenses, the policyholder will pay $10 out of pocket, and the insurance company will pay the remaining $90.

Platinum plans typically have low deductibles, copays, and coinsurance, which means that policyholders will pay less for medical care out of their own pockets. This can be especially beneficial for individuals who have high medical expenses or chronic health conditions that require ongoing treatment.

Like other ACA plans, the platinum plan covers essential health benefits, including preventive care, prescription drugs, and mental health services. It also covers pre-existing conditions and offers free preventive care services like annual check-ups, cancer screenings, and vaccines.

Overall, the ACA platinum plan offers the highest level of coverage and the lowest out-of-pocket costs, but it also has the highest monthly premiums. It may be a good option for individuals who anticipate high medical expenses or who require frequent medical care.

Last Trends in ACA plans

Expansion of subsidies: In March 2021, the American Rescue Plan Act was passed, which expanded subsidies for ACA plans. The law increased the subsidy amount for those already eligible and expanded eligibility to those with higher incomes. This has made ACA plans more affordable for many people.

How the Affordable Care Act Expanded Access to Healthcare Coverage for Millions of Americans

The ACA aimed to expand access to healthcare for Americans and to address the rising costs of healthcare.

One of the key components of the ACA was the creation of health insurance marketplaces, where individuals and small businesses could shop for health insurance plans. These marketplaces offered a variety of plans, including ACA plans, which were designed to be affordable and provide comprehensive coverage.

Before the ACA, many Americans struggled to access affordable health insurance. Insurance companies were allowed to deny coverage or charge higher premiums based on an individual's health status, and many plans had caps on coverage, meaning that individuals could quickly run out of coverage for expensive medical treatments.

The ACA addressed these issues by requiring insurance companies to cover pre-existing conditions and by prohibiting them from charging higher premiums based on an individual's health status. The law also mandated that all health insurance plans sold on the marketplaces provide essential health benefits, such as preventive care and prescription drug coverage.

Since its implementation, the ACA has faced several legal challenges and attempts at repeal by Republican lawmakers. However, it has also provided healthcare coverage to millions of Americans who previously lacked insurance. ACA plans continue to be an important option for individuals and small businesses seeking affordable health insurance coverage.

PHOTO: www.chicagotribune.com

Funding the ACA: How the Affordable Care Act is Financed

The Affordable Care Act (ACA) is primarily funded through a combination of taxes, fees, and cost-saving measures. These funding sources help to subsidize the cost of healthcare coverage for individuals who cannot afford to purchase insurance on their own.

One of the primary funding sources for the ACA is the individual mandate, which requires individuals to either have health insurance or pay a penalty. The mandate was repealed in 2019, but it was in effect for several years and generated significant revenue for the ACA.

Another funding source for the ACA is the employer mandate, which requires certain large employers to offer health insurance to their employees. Employers who do not comply with the mandate may face penalties.

The ACA also includes several taxes and fees that help to fund the program. For example, the law imposes a tax on high-income earners, as well as a tax on certain medical devices.

In addition to these funding sources, the ACA includes several cost-saving measures that aim to reduce the overall cost of healthcare. For example, the law includes provisions to encourage the use of electronic health records and to promote preventive care, which can help to reduce the need for more expensive medical treatments.

Overall, the funding for the ACA is designed to be a combination of public and private sources. The goal is to provide access to affordable healthcare for all Americans, regardless of their income or health status, while also ensuring the long-term sustainability of the program.

Last Trends in ACA plans

Increased enrollment: Despite challenges posed by the COVID-19 pandemic, enrollment in ACA plans has remained strong. In the 2021 enrollment period, over 8 million people enrolled in plans through the federal marketplace, an increase from the previous year.

Administering ACA Plans: Key Players and Processes

The administration of the Affordable Care Act (ACA) involves several key players at both the federal and state level. Here is a brief overview of how ACA plans are administered:

- Federal government: The federal government is responsible for overseeing and enforcing many of the key provisions of the ACA, such as the creation of health insurance marketplaces and the implementation of regulations related to healthcare reform. The Department of Health and Human Services (HHS) is the primary federal agency responsible for administering the ACA.

- State governments: While the federal government oversees many aspects of the ACA, each state is responsible for implementing certain aspects of the law within its own borders. For example, states are responsible for creating their own health insurance marketplaces or deciding to use the federal marketplace instead. They are also responsible for implementing regulations related to Medicaid expansion and other ACA-related programs.

- Health insurance companies: Health insurance companies play a critical role in administering ACA plans, as they are responsible for creating and offering health insurance plans that comply with the law's requirements. This includes offering essential health benefits and ensuring that all plans meet certain cost-sharing requirements.

- Healthcare providers: Healthcare providers, such as hospitals and doctors, also play a role in administering ACA plans. They are responsible for providing healthcare services to individuals who are covered by ACA plans and for submitting claims to insurance companies for reimbursement.

- Individuals: Finally, individuals themselves are responsible for administering their own ACA plans. This includes shopping for and enrolling in a health insurance plan, paying premiums, and utilizing healthcare services as needed.

Overall, the administration of ACA plans involves multiple stakeholders and requires coordination between federal and state governments, insurance companies, healthcare providers, and individuals. The goal is to ensure that all Americans have access to affordable, high-quality healthcare coverage.

PHOTO: news.stonybrook.edu

Distinguishing Between ACA and Non-ACA Health Insurance Plans: What You Need to Know

The main difference between ACA and non-ACA plans is the level of coverage they provide and the protections they offer. ACA plans, also known as qualified health plans, are required by law to provide a minimum level of coverage, known as essential health benefits. These benefits include services like preventive care, prescription drugs, and maternity care. ACA plans must also cover pre-existing conditions and cannot charge higher premiums based on a person's health status or gender.

Non-ACA plans, on the other hand, may not provide the same level of coverage or protection. For example, they may not be required to cover essential health benefits or pre-existing conditions. They may also be able to charge higher premiums based on a person's health status or gender. Non-ACA plans may be marketed as "short-term" or "catastrophic" plans and may offer lower premiums but come with higher deductibles and out-of-pocket costs.

Additionally, ACA plans are sold on the state or federally-run marketplaces, where individuals can compare plans and prices and may be eligible for subsidies to help pay for coverage. Non-ACA plans may be sold outside of the marketplaces, and their prices may not be regulated or standardized.

Overall, ACA plans offer more comprehensive coverage and protections than non-ACA plans. However, non-ACA plans may be a more affordable option for individuals who are healthy and don't require extensive medical care. It's important for individuals to carefully consider their healthcare needs and compare plans before choosing a health insurance option.

Advantages of ACA Plans:

- Essential Health Benefits: ACA plans are required to cover essential health benefits, including preventive care, mental health services, prescription drugs, and maternity care, which non-ACA plans may not offer.

- Pre-existing conditions: The ACA prohibits insurance companies from denying coverage or charging higher premiums based on pre-existing conditions, while non-ACA plans may not cover these conditions.

- Marketplace subsidies: ACA plans to offer subsidies to help lower-income individuals pay for coverage, which non-ACA plans may not offer.

- No lifetime limits: ACA plans have no lifetime limits on coverage, while non-ACA plans may have caps on coverage.

- Guaranteed issue: ACA plans are guaranteed issues, meaning that anyone can enroll regardless of health status, while non-ACA plans may be medically underwritten and deny coverage to those with pre-existing conditions.

Disadvantages of ACA Plans:

- Cost: ACA plans may be more expensive than non-ACA plans, particularly for those who do not qualify for subsidies.

- Limited provider networks: Some ACA plans may have limited provider networks, meaning that patients may not be able to see their preferred healthcare providers.

- Coverage gaps: ACA plans may have coverage gaps for certain services, such as dental and vision care, which may be covered by non-ACA plans.

- Deductibles and copays: ACA plans may have higher deductibles and copays than non-ACA plans, which can be a burden for those with significant medical needs.

- Administrative burden: ACA plans may have more administrative requirements for enrollees, such as renewing coverage each year and reporting changes in income or family size to determine subsidy eligibility.

Overall, ACA plans offer more comprehensive coverage and protections for individuals with pre-existing conditions but may come at a higher cost and with some limitations. Non-ACA plans may offer lower premiums and more flexibility in provider networks, but may not provide the same level of coverage or protections. Ultimately, the choice between ACA and non-ACA plans depends on individual healthcare needs and financial situations.

Last Trends in ACA plans

Focus on value-based care: ACA plans are increasingly moving toward value-based care, which focuses on providing high-quality care while reducing costs. This can involve initiatives such as coordinated care, preventative services, and alternative payment models.

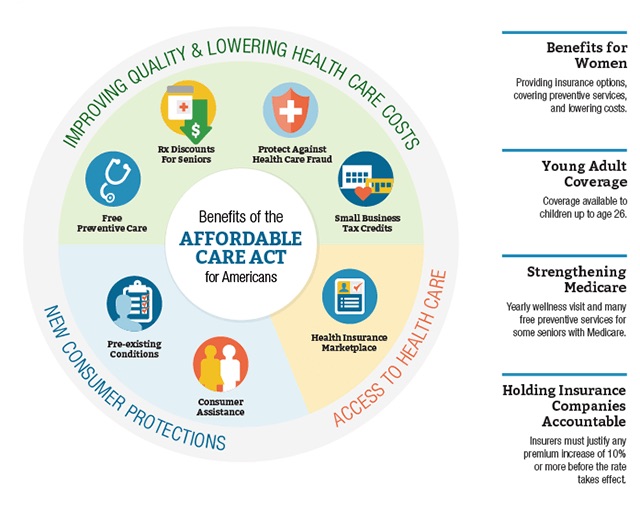

Benefits of ACA Plans

The Affordable Care Act (ACA) was enacted in 2010 to improve access to healthcare and make insurance more affordable for Americans. ACA plans offer a number of advantages and benefits, including

- Comprehensive coverage: ACA plans are designed to provide comprehensive coverage that includes essential health benefits, such as preventive care, mental health treatment, prescription drugs, and maternity and newborn care. This means that individuals with ACA plans have access to a wide range of healthcare services, without having to worry about being denied coverage for certain treatments.

- Pre-existing conditions: The ACA prohibits insurance companies from denying coverage or charging higher premiums based on a person's health status or pre-existing conditions. This means that individuals with pre-existing conditions, such as cancer or diabetes, can still get insurance coverage at an affordable price.

- Medicaid expansion: The ACA expanded Medicaid eligibility to cover more low-income Americans, providing access to healthcare services for those who may not have been able to afford it otherwise.

- Marketplace subsidies: For individuals who don't qualify for Medicaid but still need help paying for health insurance, the ACA provides subsidies to help offset the cost of marketplace plans. This makes it easier for individuals and families to afford insurance and get the healthcare they need.

- Preventive care: ACA plans are required to cover certain preventive care services, such as annual check-ups, immunizations, and cancer screenings, at no cost to the patient. This helps to catch health issues early and prevent more serious health problems from developing.

- Young adults: The ACA allows young adults to stay on their parent's health insurance plans until they turn 26 years old. This helps to ensure that young adults have access to healthcare as they transition from school to work.

Overall, the ACA has helped millions of Americans gain access to affordable, comprehensive healthcare. ACA plans offer a range of benefits and protections that make it easier for individuals and families to get the healthcare they need without breaking the bank.

Last Trends in ACA plans

Telehealth services: The pandemic has accelerated the use of telehealth services, and many ACA plans have expanded coverage for these services. This allows patients to receive care remotely, which can be more convenient and safer during a pandemic.

Limitations of ACA Plans: Understanding the Drawbacks of Affordable Care Act Coverage

While the Affordable Care Act (ACA) has brought many benefits and improvements to the healthcare system, there are also some disadvantages and limitations to ACA plans. Here are some of the main disadvantages and limitations of ACA plans:

- Limited network of healthcare providers: Some ACA plans have a limited network of healthcare providers, meaning that patients may not be able to see their preferred doctors or specialists. This can be especially challenging for patients with complex medical needs who require specialized care.

- Higher premiums: While ACA plans are designed to be affordable, some plans have higher premiums than non-ACA plans, especially for individuals who do not qualify for subsidies. This can be a significant financial burden for some individuals and families.

- Narrow coverage: While all ACA plans are required to cover essential health benefits, some plans may have limited coverage for certain services or treatments. Patients may need to pay out of pocket for some services, which can be expensive.

- Limited choice of plans: The number of ACA plans available can vary by state and region, which can limit the choices available to patients. This can make it difficult to find a plan that meets an individual's specific healthcare needs.

- Complexity: The ACA can be complex and difficult to navigate, especially for individuals who are not familiar with the healthcare system. This can make it challenging for individuals to enroll in the right plan or understand their coverage.

- Potential for policy changes: The ACA has faced legal challenges and attempts at repeal by Republican lawmakers. While the law has withstood many challenges, there is still some uncertainty around the future of the law and its provisions.

In summary, while ACA plans offer many benefits, including expanded access to healthcare and essential health benefits, there are also some disadvantages and limitations to consider. Patients should carefully evaluate their options and consider their healthcare needs and budget before selecting an ACA plan.

- ACA plans provide access to essential health benefits: The Affordable Care Act (ACA) requires that all ACA plans to cover certain essential health benefits, such as preventive services, maternity care, and prescription drugs. This ensures that individuals have access to comprehensive healthcare coverage.

- ACA plans are available on state and federal exchanges: ACA plans are available for purchase on state and federal exchanges. Individuals who meet certain income requirements may be eligible for subsidies that can help reduce the cost of coverage.

- ACA plans have limitations: While ACA plans provide access to essential health benefits, they also have limitations. For example, some plans have high deductibles and copays, which can make healthcare unaffordable for some individuals. Additionally, not all providers may be included in a plan's network, which can limit access to certain doctors and hospitals.

- The future of ACA plans is uncertain: The ACA has faced legal challenges and attempts at repeal, which have created uncertainty about the future of ACA plans. However, the law remains in effect, and millions of individuals continue to rely on ACA plans for healthcare coverage.

Questions and Answers

Where can I get information about ACA plans?

There are several resources where you can get information about ACA plans:

- Healthcare.gov: This is the official website for the federal health insurance marketplace. You can use the website to learn about ACA plans, compare plans and prices, and enroll in coverage.

- Your state's health insurance marketplace: Some states have their own health insurance marketplaces, which offer ACA plans. You can visit your state's marketplace website to learn about available plans and enroll in coverage.

- Insurance brokers or agents: Insurance brokers or agents can help you navigate the health insurance marketplace and find an ACA plan that meets your needs.

- Nonprofit organizations: Some nonprofit organizations, such as Enroll America and Families USA, offer resources and support for individuals seeking information about ACA plans.

- Government agencies: Government agencies, such as the Department of Health and Human Services, provide information and resources related to ACA plans.

It's important to note that the open enrollment period for ACA plans typically runs from November to mid-December each year, although special enrollment periods may be available for certain qualifying life events.

Who is eligible for ACA plans?

To be eligible for ACA plans, also known as Obamacare, you must meet the following criteria:

- You must be a U.S. citizen, a U.S. national, or a lawfully present immigrant.

- You must not have access to affordable health insurance through an employer-sponsored plan or a government program such as Medicare or Medicaid.

- You must not have been convicted of certain crimes.

- You must enroll during the open enrollment period, which typically runs from November 1 to December 15 each year, although some states have different enrollment periods.

- You must pay your monthly premiums to maintain your coverage.

Additionally, if you meet certain income criteria, you may be eligible for subsidies that can help lower your premiums and out-of-pocket costs. The income threshold for these subsidies varies depending on the size of your household, but generally, individuals with incomes between 100% and 400% of the federal poverty level are eligible for some level of assistance.

It's important to note that the eligibility criteria and subsidy rules for ACA plans can be complex, and may vary depending on your state and individual circumstances. If you're unsure whether you're eligible for ACA plans, you can visit healthcare.gov or your state's health insurance marketplace website to learn more and get personalized information about your options.

How to apply for ACA plans?

Here are the steps to apply for ACA plans:

- Visit Healthcare.gov: The first step in applying for ACA plans is to visit Healthcare.gov, the federal health insurance marketplace. You can also visit your state's marketplace website if your state has its own marketplace.

- Create an account: Once you're on the website, you'll need to create an account. You'll be asked to provide some basic information, such as your name, date of birth, and contact information.

- Complete the application: After you've created an account, you'll need to complete the application. You'll be asked to provide information about your income, household size, and other relevant information.

- Compare plans: Once you've completed the application, you'll be able to compare plans and prices. You can filter plans by your healthcare needs and budget.

- Enroll in a plan: After you've chosen a plan, you'll need to enroll in it. You'll be asked to provide some additional information, such as payment information and any necessary documentation.

- Confirm enrollment: Once you've enrolled in a plan, you'll need to confirm your enrollment. You'll receive confirmation via email or mail.

It's important to note that the open enrollment period for ACA plans typically runs from November to mid-December each year, although special enrollment periods may be available for certain qualifying life events. If you have questions or need help applying for ACA plans, you can contact the Marketplace Call Center at 1-800-318-2596.

How long does it take to process applications for ACA plans?

The time it takes to process an application for ACA plans can vary depending on a number of factors. Generally, you can expect to receive a determination of your eligibility for ACA plans within a few weeks after you submit your application. However, the exact timeline can depend on a variety of factors, such as:

- Completeness of application: If your application is missing information or documentation, it may take longer to process.

- The volume of applications: During peak enrollment periods, such as the annual open enrollment period, the volume of applications can be high, which can lead to delays in processing times.

- Verification of information: If the information you provide on your application needs to be verified, such as your income or household size, it can take longer to process.

- Special circumstances: If you have a special circumstance, such as a life event that qualifies you for a special enrollment period, the processing time may be shorter.

If you haven't heard back about your application within a few weeks, you can check the status of your application on Healthcare.gov or by contacting the Marketplace Call Center at 1-800-318-2596.

What information is necessary to provide to apply for ACA plans?

To apply for ACA plans, you will need to provide some personal information and information about your household. Here are some of the details you may be asked to provide:

- Personal information: You'll need to provide your full names, date of birth, Social Security numbers, and contact information, such as your mailing address, email address, and phone number.

- Household information: You'll need to provide information about your household, such as the number of people in your household, their names, and their relationship with you.

- Income information: You'll need to provide information about your income, including your gross income and any deductions you may have. You may also need to provide documentation of your income, such as a W-2 form or pay stubs.

- Current insurance: You'll need to provide information about any current insurance coverage you have, including the name of the insurance company and the policy number.

- Healthcare needs: You may be asked to provide information about your healthcare needs, such as any prescription medications you take or any pre-existing conditions you have.

It's important to provide accurate and complete information when applying for ACA plans, as this will help ensure that you're enrolled in the right plan for your needs and that you receive the appropriate subsidies if you qualify.

How is ACA different from Medicare?

The Affordable Care Act (ACA), also known as Obamacare, and Medicare are two separate healthcare programs in the United States. Here are some key differences between ACA and Medicare:

- Eligibility: ACA is available to individuals and families who do not have access to affordable health insurance through their employer or another government program, and who meet certain income and other eligibility criteria. Medicare, on the other hand, is available to individuals who are 65 years or older or have certain disabilities or medical conditions.

- Coverage: ACA plans offer a range of coverage options, including preventative care, prescription drug coverage, and coverage for pre-existing conditions. Medicare offers similar coverage options but is specifically designed to provide coverage to older adults and people with disabilities.

- Cost: ACA plans are available at a range of costs, depending on factors such as income, family size, and healthcare needs. Subsidies may be available to help reduce costs for those who qualify. Medicare is generally available at a fixed cost, based on the individual's income and other factors.

- Administration: ACA is administered by the federal government through state marketplaces, while Medicare is administered by the federal government through the Centers for Medicare & Medicaid Services (CMS).

- Funding: ACA is funded through a combination of taxes, penalties, and other sources, while Medicare is funded through payroll taxes and premiums paid by beneficiaries.

In summary, while ACA and Medicare are both designed to provide access to healthcare for Americans, they differ in terms of eligibility, coverage, cost, administration, and funding.

What are the alternatives for ACA plans?

If you're looking for alternatives to ACA plans, here are some options to consider:

- Short-term health insurance: These plans provide temporary coverage for individuals who need insurance for a limited time, such as between jobs. They typically offer lower premiums than ACA plans, but may have more limited benefits and higher out-of-pocket costs.

- Health-sharing ministries: These are organizations that allow members to share the cost of medical expenses. They are not insurance plans and do not have to meet the same requirements as ACA plans, but they can be a more affordable option for some people.

- Association health plans: These are health insurance plans offered by associations or groups, such as professional associations or chambers of commerce. They may offer lower premiums than ACA plans, but may also have more limited benefits and higher out-of-pocket costs.

- Medicaid: If you have a low income or a disability, you may be eligible for Medicaid, which is a government-run healthcare program that provides free or low-cost healthcare to qualifying individuals.

- Medicare: If you are 65 or older, or have certain disabilities, you may be eligible for Medicare, which is a government-run healthcare program that provides coverage for hospital stays, doctor visits, prescription drugs, and other healthcare services.

It's important to carefully consider your healthcare needs and budget when choosing a healthcare plan and to compare the benefits and costs of different options. Keep in mind that some alternatives to ACA plans may not offer the same level of coverage or consumer protections as ACA plans, so it's important to review the terms of the plan carefully before enrolling.