What Do You Need Earned Income Tax Credit For?

What is Earned Income Tax Credit?

The Earned Income Tax credit is designed to provide financial assistance to working individuals and families who earn a low to moderate income.

To claim the Earned Income Tax credit, taxpayers must file a tax return and submit the necessary forms and documentation. If the credit is larger than their tax liability, they may receive a refund for the difference.

The Earned Income Tax credit is an important tool for helping low- to moderate-income taxpayers make ends meet and reduce their tax burden. It is one of several tax credits available to eligible taxpayers, including the Child Tax Credit and the American Opportunity Tax Credit.

Eligibility Requirements

To be eligible for the Earned Income Tax credit (EITC) in the United States, taxpayers must meet certain requirements related to their income, filing status, and family size. Here are the general eligibility requirements for the EITC:

- Earned income: Taxpayers must have earned income from employment or self-employment. Investment income, such as interest and dividends, does not qualify.

- Income limits: Taxpayers must have earned income below certain income limits, which vary based on filing status and family size. For the tax year 2021, the income limits range from $15,980 for single filers with no qualifying children to $56,844 for married filing jointly filers with three or more qualifying children.

- Filing status: Taxpayers must file a tax return using the status of single, head of household, married filing jointly, or qualifying widow(er) with a dependent child.

- Family size: Taxpayers must have at least one qualifying child who meets certain age, residency, and relationship requirements. Taxpayers without qualifying children may still be eligible for a smaller credit.

- Social Security Number: Taxpayers and their qualifying children must have a valid Social Security number.

- Investment income: Taxpayers must have an investment income of $3,650 or less for the tax year.

- Citizenship: Taxpayers must be a U.S. citizens or resident aliens for the entire tax year.

NOTE

Eligibility for the EITC can change from year to year based on changes in income, filing status, and family size. Taxpayers who think they may be eligible for the EITC should review the most current eligibility requirements and consult with a tax professional or the IRS for guidance on claiming the credit.

How to Claim the Credit?

To claim the Earned Income Tax credit (EITC) in the United States, taxpayers must file a tax return and provide the necessary documentation to the Internal Revenue Service (IRS). Here's how to claim the credit:

- Determine eligibility: First, determine if you are eligible for the EITC by reviewing the eligibility requirements based on your income, filing status, and family size.

- File a tax return: To claim the EITC, you must file a federal income tax return, even if you are not otherwise required to file.

- Complete the EITC form: If you are eligible for the EITC, you must complete and attach Schedule EIC (Earned Income Credit) to your tax return.

- Provide necessary documentation: You will need to provide the necessary documentation to support your claim for the EITC, including:

- Social Security Numbers: You, your spouse, and all qualifying children must have valid Social Security Numbers.

- Income documentation: You must provide documentation of your earned income, such as W-2 forms or 1099 forms.

- Residency documentation: You must provide documentation of your residency status, such as a lease agreement or utility bill.

- Child-related documentation: If you have qualifying children, you must provide documentation of their age, relationship to you, and residency statuses, such as birth certificates, school records, or medical records.

- File your tax return: Once you have completed the necessary forms and provided the required documentation, file your tax return with the IRS.

- Receive your refund: If your EITC is larger than your tax liability, you will receive a refund for the difference. The IRS will issue the refund via direct deposit or by mail.

Calculating the Credit

The Earned Income Tax Credit (EITC) in the United States calculation is based on a combination of income, filing status, and family size. The credit is intended to provide financial assistance to low- to moderate-income individuals and families and can help reduce the amount of taxes owed or result in a refund if the credit exceeds the tax liability.

The EITC is a refundable tax credit, meaning that even if the credit is greater than the amount of taxes owed, the taxpayer may still be eligible for a refund of the difference. Here's how to calculate the EITC:

- Determine your earned income: The EITC is based on your earned income, which includes wages, salaries, and self-employment income.

- Determine your filing status: To calculate the EITC, you must determine your filing status as either single, married filing jointly, head of household, or qualifying widow(er) with a dependent child.

- Determine your family size: The EITC is calculated based on the number of qualifying children in your family. Qualifying children must meet certain age, residency, and relationship requirements.

- Use the EITC table: Once you have determined your earned income, filing status, and family size, use the EITC table provided by the IRS to calculate your credit. The table provides the maximum credit amount for each family size and income level.

- Calculate the credit: Using the EITC table, find the maximum credit amount for your income level and family size. Then, subtract your tax liability (if any) from the maximum credit amount to determine the amount of credit you are eligible for.

Impact on Tax Liability

The Earned Income Tax Credit (EITC) can have a significant impact on a taxpayer's tax liability in the United States. The credit is designed to provide financial assistance to low- to moderate-income individuals and families and can help reduce the amount of taxes owed or result in a refund if the credit exceeds the tax liability.

Here's how the EITC can impact a taxpayer's tax liability:

- Reducing tax liability: The EITC can help reduce the amount of taxes owed by a taxpayer. The credit is calculated based on a combination of earned income, filing status, and family size, and can be worth thousands of dollars. If the EITC exceeds the amount of taxes owed, the taxpayer may be eligible for a refund of the difference.

- Increasing refund: For taxpayers who are eligible for a refund, the EITC can increase the amount of the refund they receive. This can be particularly beneficial for low-income families who may struggle to make ends meet.

- Impact on other benefits: In addition to reducing tax liability and increasing refunds, the EITC can also impact other benefits that are based on income, such as Medicaid, Supplemental Nutrition Assistance Program (SNAP), and housing assistance. The EITC can increase a taxpayer's income, which could result in a reduction or loss of these benefits. However, the EITC is specifically excluded from income for the purposes of determining eligibility for most federal public benefits.

NOTE

The rules and calculations for the EITC can be complex, and it's possible to make errors that could delay your refund or result in penalties. If you have questions about how the EITC may impact your tax liability, consider consulting with a tax professional or using IRS-approved tax preparation software.

Changes due to COVID-19

The American Rescue Plan Act of 2021 made several changes to the Earned Income Tax Credit (EITC) in response to the COVID-19 pandemic, including increasing the maximum credit amount for taxpayers with no qualifying children, expanding the age range for eligible childless workers, and allowing taxpayers to use either their 2019 or 2020 income when calculating the credit. Additionally, the legislation temporarily expanded the child tax credit and made it fully refundable, providing additional financial support to families with children.

- The EITC is a refundable tax credit in the United States that is designed to provide financial assistance to low- to moderate-income individuals and families.

- To be eligible for the EITC, a taxpayer must have earned income and meet certain income limits, filing status, and family size requirements.

- The credit can have a significant impact on a taxpayer's tax liability, as it can help reduce the amount of taxes owed or result in a refund if the credit exceeds the tax liability.

- The EITC is specifically excluded from income for the purposes of determining eligibility for most federal public benefits.

- The rules and calculations for the EITC can be complex, and it's possible to make errors that could delay your refund or result in penalties. Taxpayers who are unsure about how to claim the credit should consider consulting with a tax professional or using IRS-approved tax preparation software.

- The EITC is an important tool for reducing poverty and improving the financial stability of low-income families, and has been shown to have a positive impact on children's health, education, and future earning potential.

FAQ

Who is eligible for the EITC?

A taxpayer with earned income who meets income limits, filing status, and family size requirements.

How is the EITC calculated?

Based on earned income, filing status, and family size, the EITC is refundable if it exceeds the tax liability.

How does the EITC impact a taxpayer's tax liability?

The EITC can reduce taxes owed or result in a refund if the credit exceeds the tax liability.

What is the maximum EITC amount?

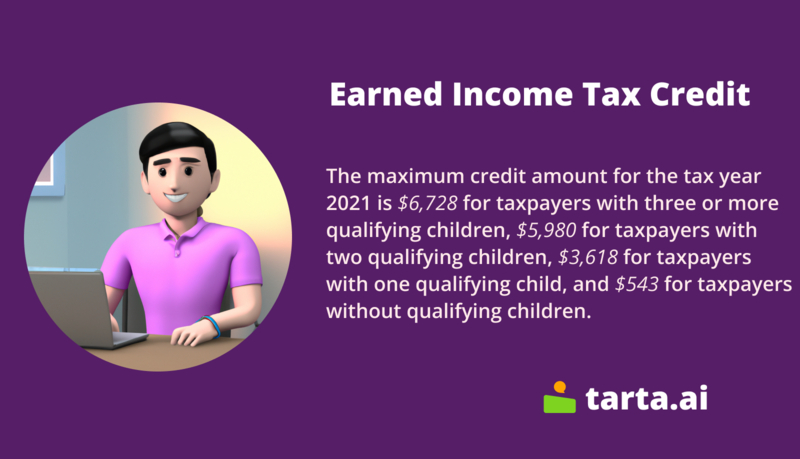

The maximum EITC varies by filing status and family size, ranging from $1,502 to $6,728 in 2021.

How can a taxpayer claim the EITC?

File a tax return and complete Schedule EIC or consult with a tax professional or IRS-approved tax preparation software.